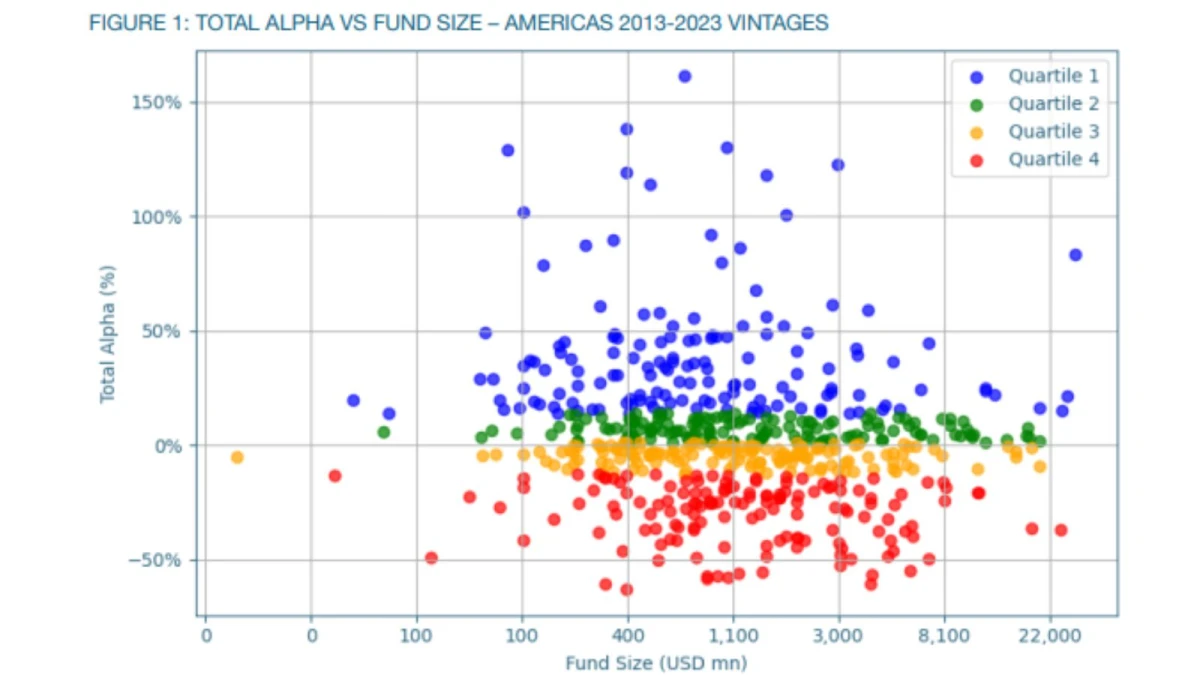

A closer look at alpha across private equity fund size

The report entitled Does Size Matter? A Closer Look at Alpha across Fund Size, analysed the performance of 586 buyout funds in North America, spanning vintages from 2013 to 2023.

The performance of the upper mid-market and large segment (excluding mega funds) was the most surprising. While many champion these segments as the higher potential parts of the market in terms of ‘alpha’ (risk-adjusted outperformance), our analysis finds that they underperformed the small, lower middle market and mega cap space.

Small and mega private equity funds outperform

Using privateMetrics® indices and the Excel plug-in tool, we calculated alpha performance across the fund universe. By segmenting funds into size buckets, we observe that smaller and lower mid-market funds achieved higher median internal rates of return (IRRs) and alpha. In the smallest bucket (< $ 500 million fund size), median alpha observed was +5.6%. At the top end of the market, mega buyout funds also produced positive alpha. Funds with greater than $ 5 billion of committed capital showed median positive alpha of 1.77%, displaying the benefits of scale at the very high end of the market.

[....]